Insurance in the Chemical Industry

Insurance in the Chemical Industry

How to Mitigate Insurance Premiums Through Safe Storage

The “exposure” factor of COPE can encompass common or special hazards. Common hazards pertain to issues like electrical system deficiencies, heating system malfunctions, and inadequate housekeeping.

Meanwhile, special hazards involve more complex risks such as flammable liquids, spray-painting operations, commercial cooking, welding, and cutting.

Depending on the type of hazards your company presents, insurance providers may require or suggest liability coverage.

Why Insurance is Critical in the Chemical Industry

Chemical businesses often face unique risks that standard insurance might not cover. General liability insurance is crucial for chemical manufacturers due to potential hazards.

Products-completed operations insurance safeguards against claims arising from chemicals, leaks, property damage, and bodily injury resulting from operations. Pollution liability and facility pollution legal liability should be considered if applicable.

Types of Insurance for Chemical Storage Facilities

● Automobile Pollution Liability if a crash/spill occurs

● Chemical Umbrella Liability

● Property – Including pollutant clean-up

● Pollution Legal Liability

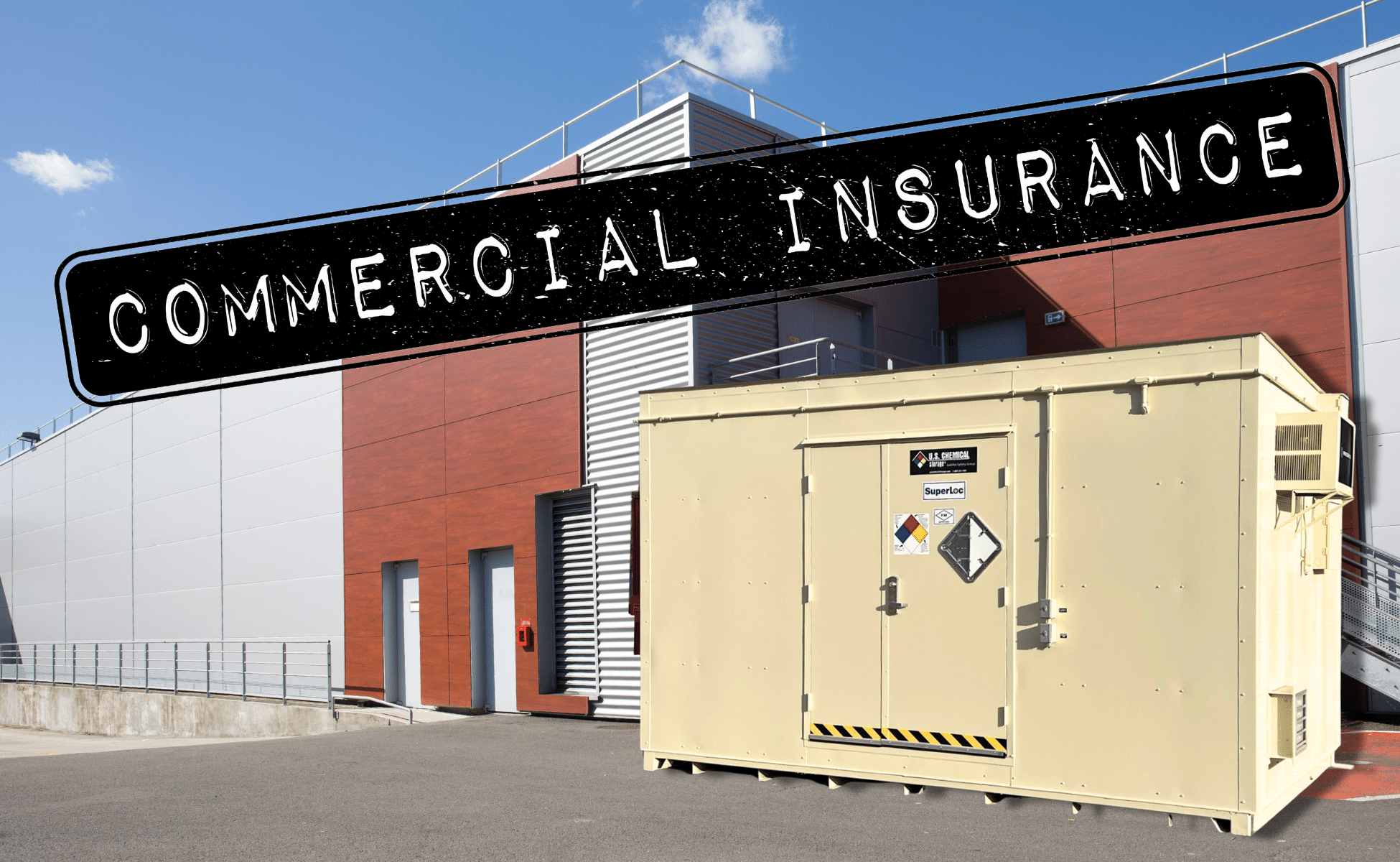

Fire Rated Storage Buildings and Insurance Savings

C: Assessing Construction & Building Adjacencies

Having a 2 or 4-hour fire-rated bi-directional (roof, floor, walls) steel structure with fire-mitigating construction to house your chemical risks is an excellent strategy for insurance coverage. Prefabricated buildings can even be placed INSIDE existing structures in many cases so efficiencies are maintained.

Information on neighboring buildings is important, too, encompassing exposed walls, hazards, construction, and proximity to danger. Buildings situated near high-hazard operations or close to flammable liquids pose significant risks.

Placing an outdoor hazmat storage building away from other essential properties may be an ideal strategy that assists in your insurance coverage.

O: Assessing Occupancy

Assigning the amount of chemicals being stored is a simple but pivotal step in determining fire risk for property insurance underwriting. This involves understanding the materials used, their proportion within the structure, and the potential fire-induced damage to the building.

Being able to organize hazmat efficiently within a fire-rated chemical storage building can help mitigate the risks and allow for easier inventories and material handling.

P: Assessing Fire Protection Systems

Private fire protection systems are vital safeguards for properties, incorporating extinguishers, alarms, and automatic sprinkler or dry-chem systems. These systems must be reliable and suitable for the chemical being stored.

Your chemical Safety Data Sheet (SDS) will point that out. U.S. Chemical Storage does the right-sizing of the fire suppression and sprinkler plan to suit the risks, with the addition of alarms, sirens, notifications, and strobes. It’s an activity we do every day, and we can easily do it for you.

E: Assessing Exposures and Natural Risks

Extra exposures like local wildfire risks, potential hurricane dangers, and proximity to flood or earthquake-prone zones also factor into risk assessment. Hurricane coverage is a misnomer. There is wind coverage, and then there is a separate flood policy. Consider both.

Natural risks are getting more common. The more aware of your risks you are, the higher your chance of getting a building that protects against them.

Using a prefabricated building that can be specifically rated for wind, snow, or seismic can allow your facility to expand in accordance with modern code, even if the rest of your facility is grandfathered.

However, other external risks could be high local crime rates, an unusually high likelihood of civil unrest, area pollution, or risks from nearby businesses or transportation. A chemical storage building with high-security features should be considered in some cases.

")

U.S. Chemical Storage Checks off Many Insurance Boxes

Regardless of when your facility was built, a prefabricated chemical storage building can help keep any hazmat you work with or produce safe and well within secure within chemical storage guidelines.

Insurance specialists and environmental consultants work with us routinely to build structures for their clients. Their goal is insurance risk reduction for hazardous materials. That is the same as our goal. With nearly any specific details or features, we manufacture and design chemical storage buildings that can serve inside or outside facilities.

Engineered Considerations

Some of the features that can improve your facility’s insurance status include:

- Fire-rated Bi-directional Construction of 2 or 4 hours (depending on the model)

- Secondary Containment Sump

- Thermal Link Dry Chem Fire Suppression

- Automatic Sprinkler Systems

- Smoke/Thermal/Radiant Heat Detector

- Gas Detectors – for a variety of gasses

- Sirens, Alarms, Strobes – with automated notifications

- Exit and Egress Features – for occupancy buildings

- Air and Cooling Units – that maintain a specific temp

- Heating Units

- Wind Rated Construction – can be higher for hurricane risk areas

- Seismic Construction – for earthquake-prone areas

- Explosion-Proof Electrical Features – to prevent sparking

- Safe and Secure Shelving and Flooring – for material handling safety

- and many more!

Insurance in the chemical industry requires a deep understanding of hazards, comprehensive coverage, and tailored solutions. By assessing risks, recommending safety measures, and providing adequate coverage, insurers play a crucial role in safeguarding businesses and mitigating potential losses. The relationship between manufacturers and insurance underwriters can be a good one through clear communication and cooperation.

Having facilities with the safety features underwriters recommend can save money on premiums now, and save environmental and safety problems in the future.

Contact us to speak with an experienced Technical Sales Engineer to assist with your storage needs